Understanding Long-Term Care Insurance Underwriting

Preparing for long-term care insurance underwriting is an essential step toward securing your financial future. The underwriting process assesses your health status and risk to determine your eligibility and premiums for long-term care insurance. Here’s a comprehensive guide to help you navigate this process effectively.

Gather Your Medical Records: The Foundation of Underwriting

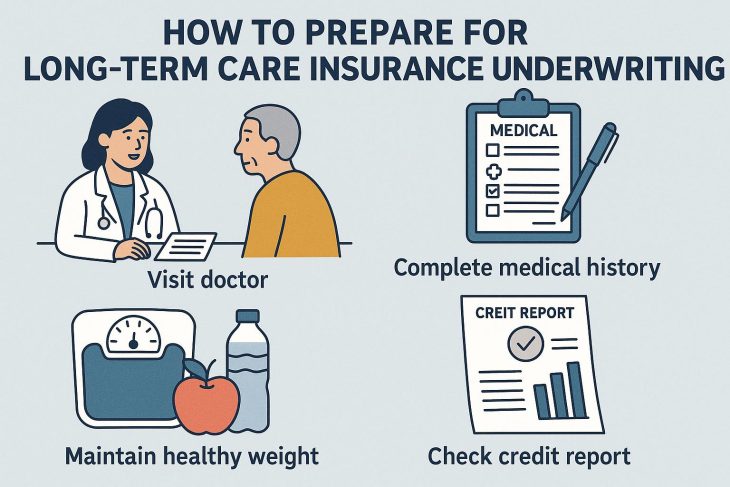

Before embarking on the underwriting process, it’s crucial to compile a comprehensive collection of your medical records. This documentation will provide the insurer with a detailed overview of your current health conditions, past medical history, and any ongoing treatments. To do this, systematically gather all your medical documentation, including records of doctor visits, health assessments, and any surgeries or treatments you may have undergone. Additionally, ensure you have your doctor’s contact information, a list of medications you are currently taking, and any recent medical tests you have completed.

Having such information readily available can significantly expedite the underwriting process. Insurers place a high value on transparency and accuracy in health documentation since it allows them to assess your risk profile more precisely. Therefore, the thorough gathering of medical records can not only smooth the process but also positively impact the evaluation.

Understand Medical Underwriting: An In-depth Examination

Medical underwriting is a critical component of the evaluation process for long-term care insurance. It involves an in-depth assessment of your health condition to establish the likelihood of your needing long-term care services in the future. During this phase, the insurer may review the medical records you have provided closely. You might also be required to undergo a medical exam or answer a series of health-related questions to verify your current health status accurately.

Understanding the specifics of what medical underwriting entails is vital to prepare appropriately. Knowing that this step will include the scrutiny of your medical past and present encourages a proactive approach. Rather than simply submitting records, consider discussing your insurance needs with your physician, who may provide insights or suggestions on managing certain conditions to better your insurance outcome.

Financial Assessment: Planning for the Long Term

Long-term care insurance underwriting considers not only health criteria but also evaluates your financial standing. Insurers seek to assess whether you can afford the insurance premiums over what could be many years of coverage. Begin by ensuring that your financial documents, such as bank statements, details of assets, liabilities, and income records, are meticulously organized and up-to-date.

This financial assessment serves a dual purpose: it affirms your ability to maintain the insurance policy and helps the insurer tailor a suitable coverage plan. Given that the premiums can be significant, part of the assessment involves evaluating your long-term financial planning, aiding in mitigating the risk of policy defaults due to financial strain. Meticulous financial preparation thus becomes an integral part of your insurance strategy.

Honesty is Key: Full Disclosure Required

When filling out your long-term care insurance application, always provide truthful and accurate information. Misrepresentation or omission of information can have severe repercussions, such as policy cancellation or claims denial at a later stage. As you complete your application, be candid about your health conditions and lifestyle habits. Misleading information, even if unintended, can lead to future complications that can disrupt your financial security.

Honesty extends beyond just medical conditions but also to lifestyle choices. Insurers may look into habits such as smoking, alcohol consumption, and even recreational activities that influence risk levels. Offering a complete and honest picture allows insurers to give fair premium rates and ensures your coverage aligns perfectly with your lifestyle and potential needs.

Review and Compare Policies: Making an Informed Decision

Understanding the different policy options available is crucial in making an informed decision about long-term care insurance. Policies can vary widely in terms of coverage types, benefit amounts, and premium costs. It’s advisable to review these policies from multiple insurers to identify the best fit for your circumstances. Consider using reliable resources such as insurance brokers or NerdWallet to compare options and find a policy that best suits your needs.

When comparing policies, pay attention to what specific services are covered, like in-home care or nursing home facilities, and evaluate the flexibility of policy terms. Some policies have more rigid terms that might restrict benefits to particular facilities or geographical locations. Thoroughly reviewing these aspects ensures that the selected policy aligns with your projected needs as you age.

Consult a Professional: Expert Guidance

Given the complexities involved in long-term care insurance underwriting, consulting a professional can be highly beneficial. An insurance advisor or financial planner can offer personalized advice tailored to your specific situation. With the multiple components of protection, such as elimination periods, daily benefits, and maximum policy limits, having expert guidance can offer clarity. They can help you understand policy terms, conditions, and the potential impact on your financial plans, ensuring that you make a well-informed and financially sound decision.

A professional can also provide insights into leveraging tax benefits associated with long-term care insurance. Often, premiums can be deductible on federal or state tax returns, subject to certain limitations. A consultant can help navigate these complex regulations and optimize your tax strategy.

Prepare for Potential Interviews: Be Ready

In some circumstances, insurers may request an interview either in person or over the phone to clarify details and ask additional questions regarding your application. Prepare for these interviews by reviewing the information you have submitted and being ready to provide explanations or further detail on any part of your application if required.

Approaching this step with preparation and clarity enhances your credibility as a candidate for insurance coverage. This is also an opportunity to express any specific concerns or requirements that you may wish the insurer to consider. Such dialogue builds transparency and potentially favorable terms in your policy agreement.

Monitor Your Health: Proactive Health Management

Monitoring and maintaining optimal health can have a positive influence on your underwriting outcome. Engage in maintaining regular check-ups, adhering to a balanced diet, regular exercise, and managing any chronic conditions effectively. Demonstrating a proactive approach to health can often positively impact how insurers assess your risk profile.

Healthier individuals typically garner better terms and more affordable premiums. Initiating lifestyle changes, such as quitting smoking or losing weight, can be leveraged to negotiate better policy conditions, underscoring the tangible benefits of sustainable health practices on insurance underwriting.

Understand Policy Regulations and Riders: Enhancing Coverage

Before making a final decision, it’s essential to understand state-specific regulations and available policy riders that can enhance your coverage. For instance, some policies offer inflation protection, a valuable rider that adjusts benefits based on cost-of-living increases, which is crucial for long-term assurance of coverage adequacy. Investigating these options requires careful evaluation of initial costs versus projected needs and benefits in later life stages.

In conclusion, diligent preparation and a thorough understanding of the underwriting process are crucial in successfully securing long-term care insurance. By being organized, deliberate, and proactive, you can significantly improve your chances of approval and find a policy that meets your financial and health needs.<|vq_7121|>

This article was last updated on: May 17, 2026